Semicap Company Pick: Advanced Packaging Play

Market Consensus Undervalues Stock Due to Anchoring Bias

Hi Everyone,

Thanks for your patience, I was consumed with planning the FinTwit Summit the past few weeks but have finally gotten to analyzing what I feel is a unique investment opportunity. I have put together an Executive Summary that lays out my current thesis, as well as a financial model that you can review at your leisure. I included a brief description of the company and industry for your reference, although I have a lot more to include there. Note: I will follow up this newsletter with the remaining company, industry, and other analyses. I wanted to get this in your hands ASAP since I think this company is positioned for a move higher.

Please feel free to shoot me a message on Twitter or email if you have any questions in the interim. I could not be more bullish on the semiconductor space, and the theme this company benefits from is the only path forward for the industry. Commentary from industry participants is just astounding, yet the market doesn’t seem to be paying attention.

You can download the financial model here. The password is the same password used to access articles on the website, which you received in your welcome email. I will follow up as soon as possible with the supplemental information around the company and industry. What’s important is the Exec Summary below.

Please make sure to share this newsletter, share this post, or subscribe (if you have not already) if you like the content! You can use the buttons here to do so:

DISCLAIMER:

All investment strategies and investments involve the risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.

Executive Summary

Company Overview

Company Name (Ticker): Kulicke & Soffa Industries, Inc. (NASDAQ:KLIC)

Market Capitalization/Price*: $2.9B/$46.42 (62.1MM shares O/S)

Business Model/Product Lines: Advanced Packaging ("AP"), Advanced Display (Mini & Micro LEDs), Aftermarket Products & Services, and Other Electronic Assembly/Trailing Edge Equipment

*Market Close 03/26/2021

Fundamentals (LTM & Q1'21; FY 2021 Consensus/Forecast)

Revenue: $746.7MM LTM (+41.7% YoY) & $267.9MM (+85.6%); $1.11B (+78.44%) / $1.17B (+87.4%; 5.4% beat)

Diluted EPS: $1.39 (+408%) & $0.77 (+266.7%); $3.20 (+286%) / $3.77 (+355%; 17.8% beat)

Free Cash Flow: $85.6MM & $38.7MM; $53.9MM / $200MM (17.2% Margin; 271% beat)

Valuation

P/E: LTM - 22.6x; YTD Annualized - 10.3x Forecast: 15x 2021 Earnings - $56 (+20.6%)

EV/EBITDA: LTM - 13.5x; YTD Annualized - 6.5x Forecast: 15x 2021 EBITDA of $285.30 - $79.73 (+71.76%)

2021 Price-Implied Expectations ("PIE"): Median - $56.81 (+13%), High - $59.69 (+19%), Low - $52.04 (+4.1%); Probability-Adjusted (60/20/20 Consensus Median/High/Low): 56.53 (+21.8%)

Differentiated Perspective

The current stock price is ~28% undervalued if the consensus outcomes is the highest probability scenario. Estimates beyond 2021 don't account for the sustainability of the company's core product portfolio or upside from KLIC's leadership in advanced packaging and dominant position in lagging edge technologies (which benefits from chip shortage, which should sustain through 2021). Importantly, estimates have not adjusted for operating leverage inherent in the updated business model. An under-investment in back-end technologies over the past several years has led to a rapid pick-up in demand for KLIC's products. A similar historical environment resulted in multiple years of above-average cash flow for the company; I believe we are entering a period of similar results for the company. The increased capital intensity required by advanced packaging techniques to accommodate multi-die packages will increase tool usage. This paradigm will lead to outperformance in the company's flip-chip and other advanced packaging product lines as heterogeneous integration becomes widely adopted in the industry. The key value factor for KLIC is volume, followed closely by operating leverage and price & mix.

Thesis

Achieve Consensus / Management Forecast: The current stock price is trading at a ~28% discount to the price-implied expectations ("PIE") valuation of $56.61 assuming an 8% cost of capital. To be clear, if the company just meets expectations, there is greater than 20% over the next 12 months. This provides a great margin of safety. It is prudent to assume the company solely achieves consensus forecasts for conservatism; however, calls with KLIC's IR and other industry insiders present a higher probability scenario of the company outperforming consensus in 2021 and beyond. Unlike prior years, the company will not experience downward seasonality in Q4 due to sustained backlog in the supply chain (more on this below).

Catalyst: Meeting $300MM revenue guidance at 20% operating margin in both FY 2021 Q2 & Q3. This should cause the market to start underwriting the base-case consensus. Additionally, a big catalyst will be FY 2021 Q4, when instead of the typical seasonality, the company reports another $300MM revenue quarter.

Chip Shipment Volumes: Kulicke & Soffa's business is highly levered to global semiconductor unit shipments, given that 75-80% of chip packages are wire-bonded and KLIC has ~60% market share in wirebonding. In the short-term, the current wirebond shortage is expected to persist throughout 2021. Within wirebonding, ~40% of KLIC shipments support multi-die packaging and 38% of all shipments are for advanced packaging equipment. The greater share of these more advanced packaging techniques represents incremental revenue and margin. The industry is expecting ~12% in total chip shipment volume in 2021; meanwhile, KLIC's guidance assumes 6.5% growth. Shipment growth over 6.5% yields more incremental revenue for KLIC (over consensus).

Catalyst: This value factor relies on 1) maintaining 38% product mix towards advanced packaging and 2) semiconductor chip shipment growth over 6.5% year-over-year.

Operating Leverage: The company's step-wise, sustainable increase in its revenue base has created operating leverage that we started seeing in FY 2021 Q1. But higher volumes are not the only cause for sustained margin expansion. Higher margins will ensue as the product portfolio towards advanced packaging equipment, the miniLED business gains traction, and incremental APS revenue falls through from a higher gross margin. The company's current business model conservatively revolves around a $1B revenue run rate and 20% operating margin; however, the "next iteration of the business model" will reflect a $1.2B revenue baseline and ~25% operating margin. However, the consensus is projecting $1.1B revenue on 18-20% operating margin. The expense structure maintains $53MM of fixed costs and 5-7% of variable costs per quarter; variable costs are inversely related to sales volumes.

Catalyst: The company needs to sustain a $1B annual revenue rate each quarter and demonstrate an operating margin of over 20% each quarter.

Risks and Pre-Mortem

Market's View on Risk: The market is applying an excessive discount to KLIC's future business prospects and ability to execute on its stated business plan. If the market continues to view the company's future cash flows as too volatile to command an average market valuation, the stock may continue to trade at a discount. However, once the company's reported results demonstrate execution and Q4 2021 does not show the typical seasonality, the stock should continue rerating higher.

Lower Capital Intensity: If its customers demand single-die packaging tools, roughly $100MM of revenue would be at risk (assuming the aforementioned 38% figure goes to 0%). The trailing-edge wirebonding business does not carry very high margins; so despite high volumes, dilution in advanced packaging shipments would drag down profitability. However, given statements by ASE (the #1 OSAT) and other industry participants, the industry is moving towards more advanced packaging, not away from it.

Semiconductor Cyclicality: The semiconductor industry is historically cyclical and KLIC's operating performance is highly dependent on these cycles. If shipment volumes retrace below 1 trillion per year, the company's profitability would follow suit. However, given demand across existing and growing electronics end-markets, semiconductor industry growth is expected to be robust for the foreseeable future.

High Beta: It's important to note that KLIC is a high beta stock (1.18 5-year monthly), a market downturn would impact KLIC more than other stocks, all else equal.

Summary

KLIC represents an opportunity to capitalize on an anchoring bias in the market. Consensus estimates have not appropriately adjusted to the company's demonstrated results and guidance. Additionally, the market is missing the upside inherent in KLIC's: 1) leadership in advanced packaging, 2) upside in automotive and memory end-markets, 3) exposure to lagging edge technologies that will benefit from the current chip shortage, 4) expected explosive growth in advanced display, and 5) evident operating leverage. The shares have ~27% upside if the company just meets consensus estimates. This indicates a high margin of safety and even further upside if the company executes on its stated business plan.

Company Details

Overview

Kulicke & Soffa (NASDAQ: KLIC) is a Semiconductor Capital Equipment ("SemiCap") company, providing equipment and tools for semiconductor, Advanced Display (LED), and electronic assembly solutions. Its end-markets include the global automotive, consumer, communications, computing, and industrial markets. Its interconnect technologies include wire bonding, advanced packaging, lithography, and electronics assembly.

These interconnect solutions enable 1) performance improvements, 2) power efficiency, 3) form-factor reductions, and 4) assembly excellence of current and next-generation semiconductor devices. The company's product excellence has made it the leader in flip-chip and other advanced packaging technologies that generate higher margins than traditional packaging. Standard packaging solutions, like KLIC's wire-bonding, is very much a commoditized product. However, higher volumes of these standard packaging tools does provide operating leverage advantages, which the company states it realizes over $1B revenue run-rates (which it is projecting for FY 2021).

The industry is entering a phase of robust secular demand driven by emerging technologies including 5G, AI, edge computing / IoT, etc. The result is a high degree of confidence among industry participants that the industry will be experiencing consistent year-over-year unit (and pricing) growth for at least the next few years. A common theme on earnings calls for players throughout the semiconductor value chain is increased visibility. KLIC specifically indicated, and I confirmed, a high level of visibility through 1H 2022 due to backlogs and ongoing order flow. This increased visibility and more stability in future results will be beneficial for the company's valuation in the market.

Industry Dynamics

Packaging Overview

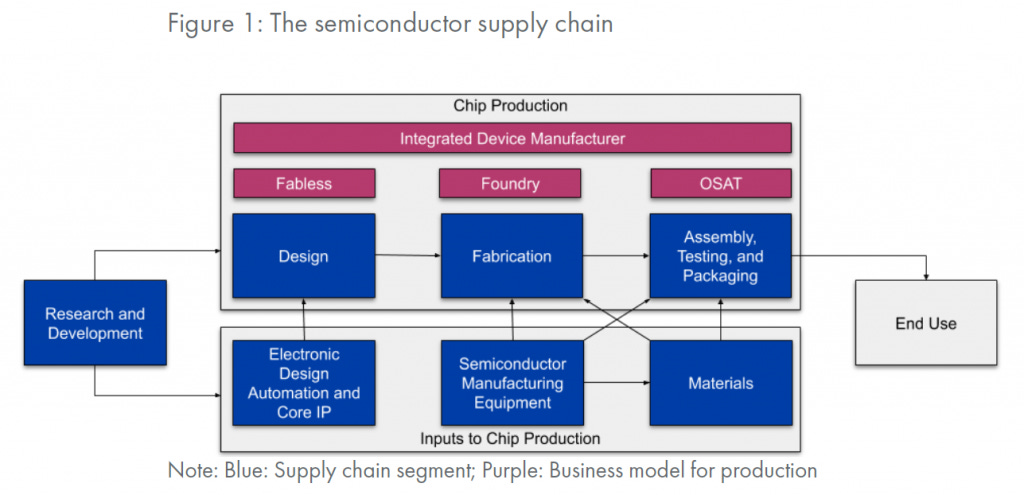

The figure above shows where KLIC sits in the semiconductor value chain; Semiconductor Manufacturing Equipment - providing equipment and tools to Assembly, Test, and Packaging ("ATP") companies. The slowdown (or end) of Moore's Law has brought the previously low-value back-end of the supply chain to the forefront. Packaging has become a bottleneck to progress in the semiconductor industry; meanwhile, the industry has begun to utilize packaging techniques to continue improving performance. People think of Moore's Law as increasing chip transistor densities; the rule of thumb being an exponential doubling every 18-24 months. While transistor densities have historically accelerated higher, chip interconnects advanced at a relatively more sluggish pace.

I'll briefly clarify the difference between transistors and interconnects. Transistors can be amplifiers or switches, the latter of which enables a binary "on" or "off" state. Transistors are organized into "logic gates" to allow computers to store information and make decisions. Interconnects do as they sound, connect transistors and other electronic components to each other, making them functional. The analogy provided by Semiconductor Engineering equates interconnects to a highway. Just as the speed at which you can drive depends on how packed the highway is, so does chip speed depend on how fast signals and power can move around the chip. So, as the quantity of transistors has increased, chip speed has been suppressed because of the lack of sufficient interconnects.

Moore's Law has served as a guiding beacon for the industry for over 50 years (which was led by Intel for the majority of that time). However, with the rate of increasing transistor densities slowing dramatically due simple to boundaries created by physics, the industry has pivoted to focusing on AP techniques to drive advancements in performance, power consumption, and form factors. There is value to learning the history of packaging, which is helpful for understanding where the industry is moving. While I will cover the essential properties, Mule on Twitter wrote a great primer on the history of packaging (note: this is part of his paid newsletter. I don't believe he is opening up to new subscribers for the time being.) I've said it a few times in this newsletter, Mule is one of the best semiconductor analysts I follow. I hope to develop his level of domain knowledge at some point in the future!

Why It's Important

I alluded to the fact that packaging is no longer taking a passive role in advancing overall semiconductor technology. While limits on transistor density is the commonly cited headwind for the industry's ability to maintain geometry scaling (shrinking everything on a chip), the bigger issue has become interconnect (the pathways that connect everything). Interconnect (the "wires") account for over 50% of the path delay in modern chips. The solutions to solving this path delay are scientifically beyond the scope of this newsletter and my level of domain knowledge.