MercadoLibre, Inc. (NASDAQ: MELI) Summary Research Report

Hold Recommendation

Hi Everyone,

In this week’s edition of the Seifel Capital Newsletter, we will review an investment analysis of MercadoLibre. Those of you familiar with this newsletter might be questioning why you are receiving it on a Tuesday instead of a Friday. While I intend on sending out the newsletter every Friday, I refuse to do so unless I have completed my analysis of the company in a manner that meets my standards. I know perfection is not attainable, but excellence is the bar I set for myself and the work I do. You, as a reader, deserve this commitment from me. Analyzing the massive company that is MercadoLibre, along with the dynamic industry and macroeconomic trends affecting the company’s future prospects, took significantly longer than some of the other companies that have been featured here. As such, instead of rushing through the analysis and producing a sub-par report, I decided to continue working nonstop until the report met my standard. We made it.

As many of you know, I have historically provided the detailed reports, upon which these newsletters are based, for free. However, I have received a significant amount of feedback that has led to the decision to start charging for the detailed versions. This decision is a result of the amount of detail, level of high quality information, and granular analysis that comprise each of these reports. I hope you all agree. You can purchase the 53-page detailed investment analysis of MercadoLibre for $49.99 by clicking on the link. Here is a link to my online store where you can purchase the detailed reports of companies previously featured in this newsletter. As a show of good faith, I am offering a money back guarantee if you review the detailed report and disagree with the quality of the analysis.

Please make sure to share this newsletter, share this post, or subscribe (if you have not already) if you like the content! You can use the buttons here to do so:

DISCLAIMER:

All investment strategies and investments involve risk of loss. Nothing contained in this website should be construed as investment advice. Any reference to an investment's past or potential performance is not, and should not be construed as, a recommendation or as a guarantee of any specific outcome or profit.

With that, please enjoy this report on MercadoLibre, Inc.!

Investment Overview

Executive Summary

MercadoLibre, Inc. (“MELI” or “MercadoLibre”) is democratizing commerce and generating financial inclusion throughout Latin America (“LatAm”). It has developed the largest online commerce and payments ecosystem in the market and has become the dominant e-commerce player in LatAm, a region with massive industry tailwinds but also significant risks. The tailwinds that will provide massive organic growth for the company include: 1) overall e-commerce penetration (LatAm is currently ten years behind the U.S. in terms of e-commerce adoption), 2) increase in overall internet usage, and 3) increased proportion of internet users who are online buyers. MercadoLibre will be the primary beneficiary as LatAm catches up to the rest of the world on these three fronts, resulting in growth of digital buyers, the majority of which will join the MercadoLibre ecosystem. The company has an excellent and highly competent management team, led by Marcos Galperin, which continues to innovate and invest in its ecosystem to maintain its competitive advantage and improve its overall offering. The company recognizes the long-term opportunity in its market and is sacrificing short-term profits by investing heavily in its platform to grow its market share (user base) for long-term success. While macroeconomic risks will challenge the company’s future prospects, the aforementioned tailwinds should fuel the company’s success into the future.

Company Overview

MercadoLibre, Inc. has developed the largest online commerce and payments ecosystem in Latin America. While it started as simply an online marketplace, the company now delivers e-commerce and digital & mobile payments solutions to buyers and sellers (“Customers”) through integrated technology verticals across the entire value chain of commerce. The virtuous ecosystem is predicated on the company’s belief that entrepreneurs are the true agents of change. To capitalize on this belief, the company promotes what it calls the Entrepreneurial Effect. The Entrepreneurial Effect is how Mercado Libre promotes individuals and companies who generate a positive “triple impact”: for business, communities, and the planet.

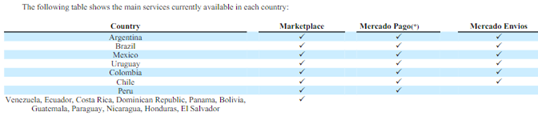

MercadoLibre operates in 18 countries including: Argentina, Brazil, Mexico, Colombia, Chile, Venezuela and Peru. It is the market leader based on unique visitors and page views in each of the major countries in which the company has a presence. MercadoLibre is elevating the broader Latin American economy through its online commerce platform and related services. Customers benefit from robust online commerce and payments tools that contribute to the development of a large and growing ecommerce community in Latin America, as well as promoting entrepreneurship and social mobility. The company has a large and untapped target addressable market (“TAM”). Latin America contains a population of over 655 million people and has one of the fastest-growing Internet penetration rates in the world yet is still lagging behind other economies. The company’s “main focus is to deliver compelling technological and commercial solutions that address the distinctive cultural and geographic challenges of operating an online commerce and payments platform in Latin America.”

Business Segments: Customers benefit from an ecosystem of six integrated e-commerce and digital payments services, all focused on expanding the ability to buy, sell, pay, deliver items, and access credit on the Internet.

Mercado Libre Marketplace: Fully-automated, user-friendly, and topically-arranged online commerce platform, which enables both businesses and individuals to list products and execute the entire sales process online.

Mercado Envios (Logistics service): Enables sellers on the platform to utilize third-party carriers and other logistics services providers. Mercado Envios provides both fulfillment and warehousing services.

Mercado Libre Advertising: Enables businesses to promote their products and services on the Internet through MercadoLibre.

Mercado Libre Classifieds: Online classified listing service through which users can list and purchase bigger ticket items like motor vehicles, real estate, and services.

Mercado Shops (online webstores solution): Allows users to set up, manage, and promote their own online stores. These stores are hosted by Mercado Libre and offer integration with the rest of the ecosystem, namely marketplaces and payment services.

Mercado Pago (FinTech platform): Integrated payments solution for online and offline, marketplace and non-marketplace transactions. It was developed to provide a better user experience and synergies within the ecosystem. Mercado Pago includes:

Mercado Credito: Mercado Libre’s credit solution, which provides cash advances and loans to sellers and buyers.

Mobile Point of Sale (mPOS): This product allows merchants or individuals to process physical credit and debit cards (offline).

Digital Wallet: The Wallet allows users to make payments, peer-to-peer (“P2P”) transactions, cell phone top-ups, and more with an account balance or with traditional payments methods.

Merchant Services: This service is designed to meet the growing demand for internet-based payments systems in Latin America, allowing merchants to facilitate checkout and payment processes either by registering with Mercado Pago or by providing their credit card information as a “guest user”.

Mercado Fondo: An asset-management feature that enables users to invest in low risk assets through their digital wallet

Industry Overview

Market Opportunity

Overview

The COVID-19 pandemic provided an inflection point in Latin America’s online consumer behavior. Many people resorted to online shopping, something a large cohort of the population previously refused to participate in, as a result of being confined to their homes. Online sales in Latin America grew by 230% during the first weeks after the declaration of the pandemic. This change in behavior seems to be a permanent shift in consumer buying activity and is becoming a normal habit in people's everyday lives. According to a survey conducted between March and April 2020, as much as 78% of the Latin Americans surveyed said they would continue shopping online after the pandemic. [Statista]

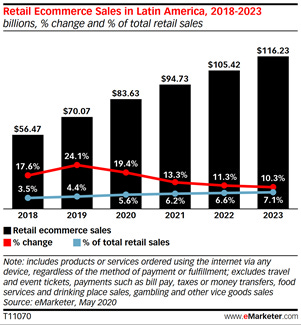

According to e-Marketer, retail e-commerce sales in Latin America will grow by an estimated 19.4% in 2020, mostly as a result in the increased online shopping during government-mandated consumer lockdowns from March through June. They do expect near-term headwinds for the retail industry as a whole, forecasting a 5.3% contraction in total retail sales to $1.506T, with recovery rates varying by market but an expected return to pre-pandemic levels by mid-2022. However, the pandemic has been a major tailwind for e-commerce. “The implications of the pandemic are far-reaching and signal a watershed moment for ecommerce in Latin America. We estimate that 10.8 million consumers will make a digital purchase for the first time this year. This will bring the total digital buyer count to 191.7 million, or 38.4% of the region’s population ages 14 and older.” Thus, despite the overall retail headwinds, retail e-commerce sales is expected to grow 19.4% to $83.63 billion. This is nearly a 7% increase in e-Marketer’s 12.5% growth estimated in its Q4 2019 forecast.

E-Commerce

In 2019, it is estimated that LatAm harbored 267.4 million digital buyers (out of a population of 655 million - only 40.8%), a figure forecast to grow over 31% by 2024 (350.3 million). Total LatAm e-commerce sales are expected to reach ~$84 billion in 2020 and $116 billion by 2023, resulting in a 12% CAGR over that time period. There exists enormous potential for future e-commerce growth in the region, which will drive expansion of the Mercado Libre Marketplace for the next few decades. E-commerce sales represented just 4.4% of all retail sales in Latin America in 2019 and is only expected to account for 6.6% of all retail sales in 2022. For comparison, e-commerce sales in the United States made up 16.1% of total retail sales as of Q2 2020. The United States had 4% e-commerce penetration over ten years ago, which has two implications for Latin America. On one hand, they are drastically behind the more developed countries. However, it also means the region has a long runway of growth potential, of which Mercado Libre will be the main beneficiary as the market leader. With $14.0 billion GMV in 2019, Mercado Libre seems to have 20% of the total LatAm e-commerce market.

Mercado Libre is the dominant leader in Brazil, Mexico, Argentina, Colombia, and Chile. These five countries comprise roughly 86% of the e-commerce market in Latin America combined. Juxtaposed to Mercado Libre’s revenue composition, this is even a bigger benefit for Mercado Libre, as 94% of its Q2 2020 Commerce revenue came from Brazil, Argentina, and Mexico alone.

Digital Payments

According to the 2020 WorldPay Global Payments Report, Latin America ranked lower than any other region of the world in terms of digital/mobile wallet penetration in 2019. Digital/mobile wallet payments represented just 2% of in-store spend and 14% of online spend. Cash was still the most common form of payment in stores, comprising 58% of total spend in brick-and-mortar locations. Credit cards were the most common form of online payment, representing 44% of total spend. According to Cell Point Digital, 85% of transactions in Latin America are cash-based and only 39% of the population has a bank account.

Once again, this paradigm reveals a massive and mostly untapped market for digital payments in Latin America. This is where Mercado Pago and the Digital Wallet will capitalize. In fact, industry reports show an ongoing transition towards digital payment methods. Overall, cash payments are expected to decline by 15% through 2023. That is just the beginning though, as it will still represent the majority of in-store payments at 43.2%. This represents a great opportunity for MELI to grow its mPOS business. Additionally, digital/mobile wallet payments are forecasted to only comprise 5.3% of in-store spend and 18% of online spend by 2023, representing a 22% CAGR and 7% CAGR, respectively. Even with the great growth forecast over the coming years, the company will have a long runway of continued growth in this area of the economy.

Main Competitors:

E-Commerce: Amazon, Walmart, AliExpress, Falabella, Americanas

Digital Payments: PayPal, PagSeguro, StoneCo

Investment Thesis

Current Overvaluation: The stock has appreciated 84.8% over the past year and 136% since its March low of $422.22. As a result, the company currently has valuation multiples significantly higher than its peer group, as discussed in the comparable companies analysis. Multiple reversion is a risk for the company’s stock performance.

Network Effects: MercadoLibre is building an ecosystem that effectively drives user engagement and benefits from strong network effects. The more users there are on the online marketplaces, the more sellers there are, which lead to more users (flywheel). With MercadoPago, especially with off-platform transactions, the more merchants there are that accept MercadoPago, the more users there will be, leading to even higher merchant-acceptance (flywheel).

Nascent E-Commerce and Digital Payments Industries in LatAm: LatAm is nearly a decade behind the U.S. in terms of e-commerce adoption. During Q2 2020, online sales accounted for about 16% of total retail sales in the U.S., up from about 4% 10 years ago. In Latin America, e-commerce comprises only 4.2% of total retail in the region. It’s evident that MercadoLibre has a longer organic runway in LatAm than Amazon has in the U.S., as the entire region catches up with the developed world. In addition to e-commerce penetration, the growth in internet users as a percentage of the population, as well as the percentage of those users who are also internet buyers, will provide the company a growth runway for many years to come.

Strong Industry Tailwinds: According to Statista, it is estimated that there were 267.4 million digital buyers in Latin America in 2019. This figure is forecast to grow over 31% by 2024 (350 million). Although the adoption of e-commerce in Latin America is still lower than in other emerging regions, online retail sales generated more than $70 billion U.S. dollars in 2019 and are expected to hit $116 billion by 2023.

Demographic Tailwinds: Latin America represents a larger TAM for Mercado Libre than the U.S. does for Amazon or eBay, as the region is home to 655 million people, compared to just 331 million in the U.S.

Leader in Biggest Markets: MercadoLibre is the leader in e-commerce in Brazil, Mexico, Argentina, Colombia, and Chile, which together account for ~86% of online sales in Latin America. According to Statista, Brazil and Mexico compete for the majority of the share, accounting for 32.5% and 28.8% of the Latin American e-commerce market, respectively. With GMV of $14 billion in 2019, MercadoLibre accounted for roughly 20% of the e-commerce market in Latin America .

Innovation: The company’s history of innovation is profound. After launching as an online marketplace in 1999, the company has added Mercado Pago, Mercado Envios, Mercado Credito, Mercado Fondo, and more to create the premier e-commerce ecosystem in Latin America.

Management: Chairman, President, and CEO Marcos Galperin co-founded the company in 1999 while studying at Stanford Business School. He holds 8% of the company’s shares in a trust; he is personally invested in the company’s success. MercadoLibre’s dominance in the market and success, thus far, of rolling out its logistics solution, are signs of a quality management team.

Investment and Growth Strategy: MercadoLibre is sacrificing short-term profits to execute on a long-term vision, by investing heavily in S&M and its logistics infrastructure to gain market share, which will result in future profitability and growth.

Macroeconomic Risks: The company is subject to significant political and economic risks that continue to impact the entire region. The downfall of Venezuela caused the company to take impairment charges and then eventually deconsolidate the business unit. Additionally, widespread high inflation and a weak currency diminishes the business’ success on a USD basis. Juxtaposing growth trends on a USD and FX neutral basis highlights this pernicious impact.

Investment Framework

Critical Factors: The change in financial reporting makes it difficult to understand what the street expects in terms of these four critical factors. See detailed report for a more in-depth discussion on these factors.

Number of Items Sold

Market View: Estimating the Street assumptions that drive Commerce revenue (specifically, Marketplace revenue) is mostly guess work. Thus, SCM will assume the Street shares a similar view on the growth in number of items sold.

SCM View: SCM sees the total number of unique items sold increasing from 178.5 million in Q2 2020 to 186.2 million, 197.1 million, and 204.6 million over the next three quarters through Q1 2021.

Average Price per Item Sold

Street View: SCM can infer the market is assuming a slight increase in average price per item sold, based on the Street’s estimated forecast of higher average spend per transaction (see below).

SCM View: SCM assumes $30 per item sold, consistent with consumer buying patterns and recent results.

Total Payment Transactions (“TPT”)

Street View: Despite the company’s consistent growth pattern over the past six quarters, the Street seems to be expecting only 40% growth in TPT over the next three quarters. This implies an expectation that TPT will decline in Q3 and Q4 2020.

SCM View: SCM assumes 100% YoY growth for the next three quarters. This would lead to TMT of 454 million, 571 million, and 581 million for Q3 2020 through Q1 2021, respectively.

Average Spend per Transaction

Street View: The Street is making more aggressive assumptions here, indicating an estimated $29 FY 2020 average spend per transaction. This runs contrary to the declining historical trend and consumer behavior patterns.

SCM View: Average spend per transaction was $27.8 and $27.7 for Q1 and Q2 2020, respectively. SCM expects consistent performance through 2H 2020, ending the year with an average spend per transaction of $26.7 (21.3% lower than the $33.9 achieved in 2019).

Conviction Level: Why SCM view is Right

SCM believes it has a slight analytical advantage due to the more in-depth bottom-up financial modeling exercise it performs. However, there often exists an overconfidence bias as a result of granular modeling. As such, this analytical advantage may not prove to be helpful as it relates to MercadoLibre, especially given the company’s recent change in reporting structure and pop in Q2 2020 results.

Additionally, SCM believes the Street has an informational advantage given its access to management in light of the two factors mentioned above. As such, SCM does not have the highest conviction in its estimates when compared to the Street.

What is the Market Missing? Why is There a Mispricing?

The COVID-19 pandemic led to a bid in the company’s stock, as it has advanced 136% since its March lows when the broader markets sold off. The market realized the benefits that lockdowns would have on the company’s business, as rapid e-commerce growth and digitization would result as people were forced to stay and shop from home. Give the company’s current valuation, it seems the market is discounting some of the company’s key risk factors.

The Catalyst for Each Critical Factor (Calendar)

SCM is shortening its investment horizon to 6-9 months for MercadoLibre, as it will need to closely monitor the results of the critical factors identified in this report. Fiscal Year 2020 reporting should prove as the target date by which SCM and the Street will have a better understanding of MELI’s future prospects. Additionally, this will provide another year of revenue reporting in the new structure and a full year of reporting for the set of metrics the company has decided to publish.

Risk / Reward

The risks associated with investing in MercadoLibre are discussed in the detailed report. Specifically, a slowdown in growth that could result from a deceleration in adoption of the company’s e-commerce and digital payments solutions than what was experienced in Q2 is a possibility. Additionally, the company faces cultural challenges relating to digital payment adoption, in addition to the various macroeconomic risks (i.e. political, economic, currency). However, the company’s large TAM and growth runway is undeniable, providing substantial upside for the company in the future.

Pre-Mortem and Who’s on the Other Side?

Investment in MercadoLibre failed, what went wrong?

The company’s multiples revert to the mean, contracting closer to the industry average

The Q2 2020 spike in performance was a one-off event, with growth returning to pre-pandemic levels faster than expected

Major players like Amazon, Alibaba, and Walmart invest significantly more resources in the region to benefit from the untapped market, creating more competition for MELI and further diminishing ROIC

The company can’t full execute on its logistics strategy and market penetration can’t surpass 50%, resulting in a persistent drag on margins

The company has to ramp its sales and marketing expenses up again post-pandemic as organic growth wears off

Macroeconomic events trigger that hurt the company, whether they be political events or economic contractions

Local currencies continue to devalue and experience high inflation, diminishing the company’s results

Who’s on the other side of the trade and why are they selling? Why could they be right and SCM be wrong?

Participants could be selling due to the current valuation, a valid concern in SCM’s view

A more subdued growth outlook for the company could make investors pessimistic, a result that could occur from cultural frictions or increased competition

There are multiple large scale e-commerce companies that make for attractive investment opportunities, so there may not be enough room for MELI in an investor’s portfolio if they wish to diversify

Investors who are risk-averse will not want to invest in MELI due to potential left-tail events

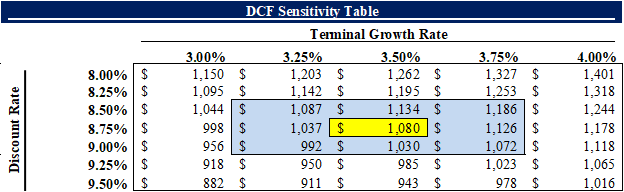

Appendix - Financial Summary and Valuation